Protracted conflict in Middle East: inflation rate close to 6%;

Credit: STATEC

Protracted conflict in Middle East: inflation rate close to 6%;

Credit: STATEC

On Tuesday 12 May 2026, the Luxembourg Government, the Union of Trade Unions, the General Confederation of Public Service, the Union of Luxembourg Businesses and the Chamber of Agriculture held the first meeting of the Tripartite Coordination Committee.

According to the Ministry of State, the purpose of this meeting was to assess the economic and social repercussions of the war in Iran, and the agenda included discussions on oil, natural gas, electricity and the European Union’s response to the crisis.

The presentation given by the Government Commissioner for Energy, Simeon Hagspiel, detailed the “Energy Triangle”, which links the influence between energy security, accessibility/cost and environmental sustainability, the balance of which is subject to constant change due to climate change and international crises.

On the subject of dependency on energy imports, the EU energy bill for fossil fuel imports was reported at €337 billion in 2025. The report detailed that fossil fuel dependence is persistent across the EU despite the volumes reducing for each country year-on-year since 2004. Notably, Luxembourg is second only behind Malta in registering the highest dependency on fuel imports (90% in 2024).

This highlights that for Luxembourg to meet its climate objectives (in accordance with the EU and the Paris Agreement) of achieving climate neutrality by 2050 and a reduction of emissions by 55% by 2030 means that considerable progress will be required. Even more so if it is to achieve its additional objectives of a 37% share of renewable energy, a 42% improvement in energy efficiency and a 49% share of electric vehicles.

In relation to the ongoing conflict in the Middle East, and in particular the Strait of Hormuz, the report said the repercussions upon the complex interdependencies are difficult to anticipate and do not manifest immediately. This is particularly impactful due to Luxembourg having no production or refining capacity for oil, being reliant on imports for 100% of finished oil products and oil accounting for 59.7% of the country’s total energy consumption (8.8% biofuels).

Globally, significant stocks have mitigated the effects and limited volatility. However, stocks are decreasing and are currently not being replenished. In Luxembourg, IEA and EU obligations meant holding 90 days of stock but also tied the country to contributing to the IEA stock replenishment in early March. In terms of pricing, global markets have seen a significant increase and extreme volatility since the beginning of the war, with price levels similar to those observed during the 2022 crisis.

At the pump, prices in Luxembourg are defined by product costs, distribution costs and taxes. Despite the maximum pricing system for petrol 95 and 98, diesel, heating oil and LPG, and competitive prices due to low taxation, certain consumers are particularly exposed (transport, logistics, commuters, etc.) to pricing fluctuations.

For Luxembourg’s Natural Gas Sector, there are relatively low stock levels due to a cold winter in 2025-2026. Despite a reduction in consumption of LNG within the EU since 2021 (-21% in 2025), the EU is competing on the global LNG market to replenish its stocks, with an obligation to fill storage facilities to 90% before winter; with a contribution from Luxembourg suppliers equivalent to 15% of their consumption.

The report noted that electricity pricing is currently at very different levels from those observed during the 2022 crisis but prices have increased from approximately €30/MWh to €61/MWh on 19 March 2026 following the conflict in Iran. As of 11 May 2026, it sits at €46/MWh. For Luxembourg and its neighbouring countries, the final MWh price includes energy, network costs and taxes and is dependent on the product and may vary considerably as a result. The price is also smoothed and delayed compared with the wholesale price because of suppliers’ purchasing strategies.

For the German-Luxembourg market price, there are repercussions from the Middle East crisis due to gas-electricity price coupling but effects have been mitigated by renewable energies and by a sharp fall in the CO2 price. However, there is increased volatility leading to the growing importance and value of networks, storage and flexibility to meet demand.

In relation to network transmission costs, the State has covered a significant part of these since 1 January 2026 and will do so for at least three years. €150 million will be invested for the year 2026 and the measure applies automatically to all customers, households and businesses.

In terms of supply, despite strong dependencies, there is currently no shortage in Luxembourg but extreme uncertainty regarding the development and scale of the crisis creates a real risk of shortages in the event of a prolonged crisis (particularly in relation to kerosene and diesel).

Overall, there has been a significant price increase for oil products, a tangible increase for gas and a slight increase for electricity so far; with increased volatility coupled with extreme uncertainty. This has created strong variation in repercussions depending on the type of consumer, with some already significantly affected.

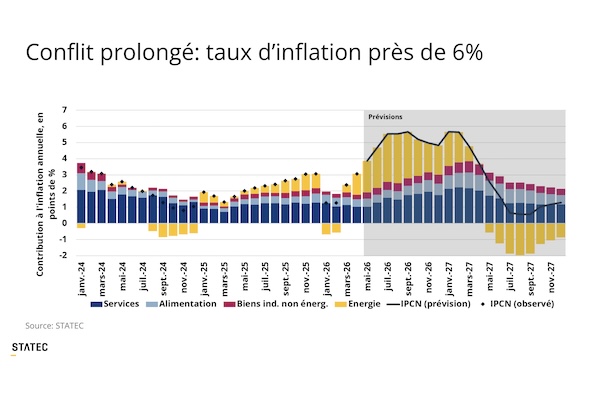

In response, Luxembourg’s national statistical office, STATEC, reported that a prolonged blockade in the Strait of Hormuz could see inflation rise to 6% and, with the conflict weighing on growth forecasts, there is the possibility of a recession in 2026.