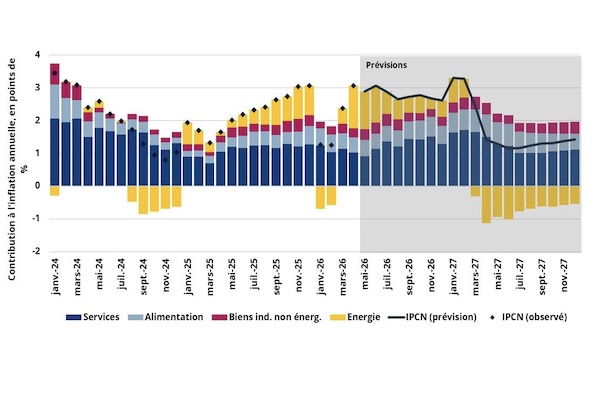

Annual inflation rate and contributions (forecasts as of Wednesday 6 May 2026);

Credit: STATEC

Annual inflation rate and contributions (forecasts as of Wednesday 6 May 2026);

Credit: STATEC

On Wednesday 6 May 2026, Luxembourg’s statistics institute, STATEC, published its updated inflation forecast along with an update the next wage indexation.

STATEC reported that after a beginning of the year marked by a decline in inflation, geopolitical tensions in the Middle East have reignited pressure on energy prices and darkened the economic outlook. Disruptions to maritime traffic in the Strait of Hormuz, a strategic route for global trade in oil and liquefied natural gas, have increased volatility in energy markets and led to a marked rise in fuel prices worldwide.

The statistics institute said that, assuming that the conflict remains limited in duration, inflation in Luxembourg would reach 2.5% in 2026, driven by a strong rebound in energy inflation. This would turn negative again in 2027, while second-round effects - notably through food prices - would continue to strengthen, bringing inflation to 1.7% in 2027.

The triggering of the next wage indexation tranche is expected this month and would be followed by a further tranche in the second quarter of 2027. Given the considerable uncertainties surrounding the international environment, developments could nevertheless fall within a wide range, spanning the different scenarios outlined by STATEC.

STATEC highlighted that the current shock remains concentrated on petroleum products for the time being, with the impact on gas being significantly more limited than in 2022. Second-round effects are, however, expected with a lag of several months, particularly via food prices: rising gas prices are passed on to nitrogen fertilisers and, through this channel, to agricultural production costs, explaining the rise in food inflation in 2027 (3.3% after 2.9% in 2026).

The international environment marked by uncertainty

STATEC said the international economic environment has deteriorated markedly in recent weeks, following the outbreak of war in Iran. In Luxembourg, these tensions are, at this stage, mainly reflected in energy products, particularly diesel and its derivatives. Between January and April, prices for heating oil and diesel rose sharply, by 78% and 45% respectively, contributing to a pronounced rebound in inflation, which once again exceeds 3% in April.

In the central scenario of the current STATEC forecast, based on Oxford Economics projections from April 2026, a ceasefire would prevent a major escalation, even though a full return to normal conditions would occur only gradually. In this context, the price of Brent crude would average $113 per barrel in the second quarter of 2026, before easing back towards $80 per barrel by the end of the year. This temporary rise in energy prices, combined with the increase in several commodity prices observed since the onset of the conflict in Iran - particularly agricultural inputs such as nitrogen-based fertilisers - would push euro area inflation to 3.3% in the second quarter of 2026, i.e. less than one third of the peak reached in 2022. The magnitude of the shock would therefore remain significantly more contained than during the previous inflationary episode. The average Brent price observed in April was close to the level expected for the second quarter, supporting this trajectory. A favourable outcome to the negotiations initiated since the ceasefire of 8 April could lead to lower prices, while a failure of the talks would result in renewed escalation—two configurations explored in the alternative scenarios.

In Luxembourg, the impact of the shock would initially materialise through inflation in petroleum products, whose prices would rise by 12.4% in 2026. Energy inflation would thus reach 6.6% in the same year, before recording a decline of a comparable magnitude in 2027, as energy prices normalise with the gradual recovery of traffic through the Strait of Hormuz. Second-round effects would then gradually emerge from late 2026 onwards, notably affecting food prices. The strong dependence on fertilisers transiting through the Strait of Hormuz plays a particular role in this transmission. Since the beginning of the conflict, prices of granular urea have increased by around 50%, while ammonia prices have risen by approximately 20%. This increase is mainly driven by higher natural gas prices, which are the primary input in the production of nitrogen-based fertilisers. Combined with the ongoing planting season in the Northern Hemisphere, this rise in agricultural input costs would be passed on to food prices with an estimated lag of 6 to 12 months, contributing to the persistence of food inflation in 2027. As a result, food inflation would reach 2.9% in 2026 and 3.3% in 2027. Finally, more diffuse effects would affect services and non-energy industrial goods, whose inflation rates would rise moderately, from 2.7% to 2.9% and from 1.0% to 1.1% respectively in 2026 and 2027. Overall, inflation in Luxembourg would amount to 2.5% in 2026 before easing to 1.7% in 2027.

According to these projections, which constitute the central STATEC scenario, the next wage indexation would take place in June 2026 (following its triggering in May) and would be followed by another tranche in the second quarter of 2027. This schedule brings forward the second tranche by one quarter compared with the February 2026 projections, which had anticipated a second tranche in the third quarter of 2027.

STATEC emphasised that given the high degree of uncertainty surrounding the international environment, the outlook remains particularly fragile and subject to rapid changes. In a context marked by strong dependence on geopolitical developments, abrupt shifts - whether in the form of escalation or, conversely, de‑escalation - could significantly alter the trajectories described. Developments could therefore fall within a wide range, lying between the central and high STATEC scenarios, or even temporarily diverging from them depending on the speed of adjustment in energy markets and the responses of economic agents.