Tax calculation basis since 2018;

Credit: MMTP

Tax calculation basis since 2018;

Credit: MMTP

Luxembourg's Ministry of Mobility and Public Works has issued a statement in which it responds to the recent opinion of the non-profit organisation Mouvement Ecologique asbl on the planned reform of company car taxation.

Earlier this month, Mouvement Ecologique had argued that government measures in the area of climate action, including those regarding company car taxation, were insufficient and risked negatively impacting financially fragile households.

In response, the Ministry of Mobility and Public Works stressed that the planned reform of company car taxation forms "part of a holistic strategy to make the national vehicle fleet more climate-neutral in the long term".

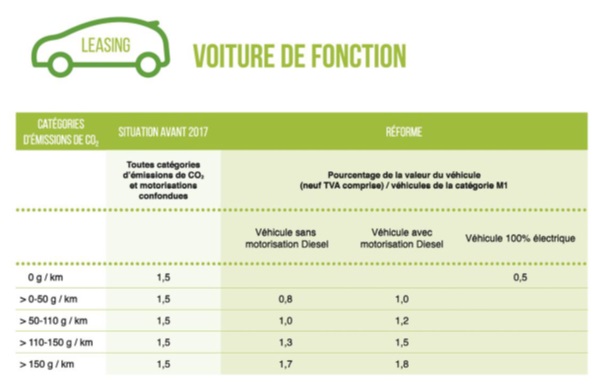

The ministry recalled that the assessment basis for the car taxation was redesigned in January 2020 due to adjustments at the European level. With the introduction of a new test cycle (Worldwide Harmonized Light Vehicles Test Procedure - WLTP) to determine CO2 emissions for light vehicles, the assessment basis for calculating vehicle tax increased by around 20% compared to the old cycle (New European Driving Cycle - NEDC). Accroding to the ministry, this adjustment was essential because the real CO2 emissions, which are directly linked to the consumption values of the vehicles, increasingly deviated from the emissions determined during the type approval, and the expected effect of CO2 reduction under real use did not occur accordingly.

In order to take these adjustments into account, in addition to the assessment basis for calculating the car tax, those for calculating the monetary benefit of a company car were also adjusted by using the new test cycle and the resulting more realistic values as a basis. The ministry thus argued that "contrary to the statement of the Mouvement Ecologique, the assessment basis for the pecuniary benefit of a company car has already been converted to the realistic WLTP measured values".

The Ministry of Mobility and Public Works added that whilst no adjustments were made to the stage model in 2020, the assessment basis was switched to WLTP, which increased it by 20%. Vehicles with internal combustion engines were therefore generally classified in the next higher tax class. It also noted that, with the planned reform, the phased model will now be adjusted in two steps in order to further favour electric vehicles in particular and to significantly reduce the upper limit for maximum CO2 emissions (from 150 g / km to 130 g / km).

Taking into account that the analysis of company cars was based on the new registrations of leased vehicles, the adjustments made in 2020 in particular appear to have had an effect on the new registrations of lower-emission vehicles, according to the ministry. This control effect is to be used in particular for the transitional period until 1 January 2025 by continuing to uphold tax advantages, especially for battery-powered electric cars.

On the other hand, for all vehicles that have CO2 emissions of more than 80 g / km, the tax base will be increased by at least 0.2%, with the maximum remaining at 1.8%. In return, however, the CO2 upper limit, from which the maximum rate applies, will be reduced by 20 g / km.

The ministry argued that this is "a clear approach to promoting electromobility and not granting any tax advantages to vehicles with high exhaust emissions".

Moreover, the ministry noted that in the second phase, from 2025 onwards, all vehicles with internal combustion engines, as well as hybrid and plug-in hybrid vehicles will ultimately be taxed on the calculation basis of 2% of the purchase value, while pure electric vehicles will be taxed at 1% and 1.2% respectively. This adjustment is aimed at making vehicles with combustion engines less attractive as company cars.

The ministry concluded that this was not a question of a state subsidy. By retaining the advantages for 100% electric vehicles, the aim is to avoid that vehicles with high CO2 emissions are ultimately financed via private leasing or are bought privately, but rather a purely electric vehicle is used and the penetration in the market is thus accelerated.