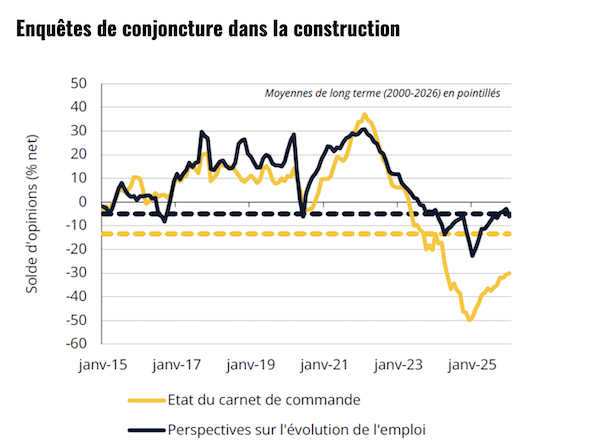

Business confidence surveys in the construction sector;

Credit: STATEC

Business confidence surveys in the construction sector;

Credit: STATEC

On Tuesday 24 February 2026, STATEC published its latest Conjoncture Flash report, highlighting an improving sentiment among construction companies in Luxembourg and emerging positive signs in the labour market.

However, activity continues to stagnate at a low level and investment trends remain mixed, with better developments in housing and weaker ones in other buildings and civil engineering works.

Employment in construction increased by 0.1% quarter-on-quarter in the fourth quarter of 2025, according to provisional data, marking the first increase in almost three years. Job vacancies have also risen in recent months, although order books remain below pre-crisis levels.

The report also pointed to broader developments in the euro area, where GDP grew by 0.3% quarter-on-quarter in the fourth quarter of 2025, bringing annual growth to 1.5%. Germany saw a consumption-driven rebound, while Spain maintained solid expansion.

It further noted that the euro appreciated significantly in 2025, strengthening by 5.3% in real effective terms, supported by a weaker US dollar and improved growth prospects in the euro area.

Inflation declined sharply in January 2026. Annual inflation in Luxembourg fell from 3.1% in December to 1.3% in January, compared with a more moderate decrease in the euro area from 2.0% to 1.7%. While the European slowdown was largely driven by lower energy prices, domestic factors, including changes to electricity tariffs and seasonal sales, also played a significant role.

Electricity prices fell substantially in January, declining by 10.5% month-on-month and year-on-year, following the state contribution to electricity network tariffs. Seasonal sales also exerted downward pressure on prices, although their overall impact remained limited due to the relatively small weight of discounted goods in the consumer price index. More pronounced reductions than usual were observed for certain items, including women’s shoes (-22% year-on-year), infant clothing (-9%) and bicycles (-7%). Price increases in services were limited in January, with notable exceptions including museums, swimming pools, fitness subscriptions and driving lessons.

The report also highlighted a rise in labour market participation among Ukrainian beneficiaries of temporary protection. In January 2026, more than 1,500 Ukrainian BPT holders were active in Luxembourg’s labour market, corresponding to an activity rate of around 50% among those aged 15 to 64, compared with approximately 75% for the overall resident population. Around 900 Ukrainian refugees were in employment, representing 0.2% of total employment, with women accounting for 60%. Nearly one quarter work in the hospitality sector, 16% in health services and 44% in other service activities. While registrations of Ukrainian jobseekers with ADEM have increased slightly, they account for only 4% of the overall rise in unemployment since August 2025.

Beyond labour market developments, the report also examined trends in the financial sector. The banking sector continued its long-term consolidation. At the end of 2025, Luxembourg had 116 active credit institutions, compared with 156 in 2005, representing a 26% decline over 20 years. Despite the reduction in the number of banks, total assets increased by 24% over the same period, equivalent to nearly €200 billion. In 2025, banking assets grew by 2.5%, supported by lower interest rates and a rebound in credit demand, while employment in the sector remained broadly stable (+0.4%). Demand for IT development, technical support and systems administration profiles remains strong, alongside increasing vacancies in credit and risk analysis, financial engineering and client management.

Credit demand showed mixed developments in the fourth quarter of 2025. Consumer loans and business loans increased by 8% and 3% quarter-on-quarter respectively, while mortgage lending declined by 17%. Mortgage volumes had previously surged in late 2024 and mid-2025 ahead of the expiry of several housing support measures. Interest rates on new loans have eased compared to mid-2023, standing at 4.2% for consumer credit and 3.3% for mortgages, supporting household demand amid improved property market prospects. Business credit remains well below pre-rate-hike levels but is expected to recover gradually in early 2026.

Regarding European climate policy, STATEC highlighted growing uncertainty surrounding the EU Emissions Trading System (EU ETS). Following strong price increases after the post-COVID rebound and energy crisis, emission allowance prices exceeded €90 per tonne of CO₂ in mid-January 2026 amid expectations of reduced free allocations in 2026. However, discussions of potential reforms contributed to a rapid correction, with prices falling by more than 20% within one month by mid-February.

Recent key indicators show Luxembourg’s nominal GDP reached €86.18 billion in 2024, the current account balance stood at €1.802 billion in the third quarter of 2025 and the consumer price index reached 1,022.30 in January 2026.