GDP in volume (Source Eurostat, STATEC);

Credit: STATEC

GDP in volume (Source Eurostat, STATEC);

Credit: STATEC

On Wednesday 24 June 2026, STATEC published its latest Conjoncture Flash report, indicating that Luxembourg’s GDP growth remained unchanged in the first quarter of 2026.

In the report, STATEC said that Luxembourg’s GDP stagnation in the first quarter reflected a range of factors but on closer examination of the figures, revealed a less negative picture than may initially appear.

According to STATEC, economic activity held up relatively well in both the euro area and Luxembourg during the first quarter, despite seemingly disappointing headline results. However, economic momentum is expected to weaken in the second quarter due to tensions arising from the closure of the Strait of Hormuz, some of whose effects may persist even if the waterway reopens.

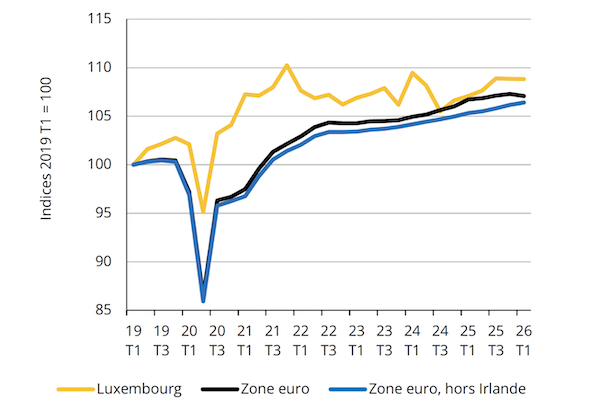

GDP figures for the first quarter of 2026 appeared lacklustre in both the euro area and Luxembourg. Euro area GDP contracted by 0.2% quarter-on-quarter, while Luxembourg's GDP remained unchanged.

June 2026: a situation not yet resolved

STATEC said the decline recorded in the euro area was largely attributable to Ireland's performance (-12% quarter-on-quarter), once again heavily distorted by the volatile activities of multinational corporations based there. Excluding Ireland, euro area GDP would have grown by 0.2% quarter-on-quarter, broadly in line with the pace recorded in the fourth quarter of 2025. Performance nevertheless varied considerably among the major Member States. Economic activity strengthened in Germany (+0.3%, compared with +0.2% in the previous quarter), supported in particular by a rebound in exports and public consumption expenditure. Italian GDP also increased by 0.3% (the same as in the previous quarter), while Spain's economy slowed somewhat (+0.6%, following +0.8% in Q4 2025). France, by contrast, recorded a slight contraction (-0.1%).

In Luxembourg, GDP stagnation in the first quarter reflected a range of factors. Industrial value added made a particularly negative contribution to overall performance, mainly due to a decline in capital goods production (partly as a correction following a very strong increase at the end of 2025). Financial activities also weighed on growth, although to a lesser extent. By contrast, several branches of the market sector—which had either stagnated or performed poorly in previous quarters—regained momentum at the start of 2026, notably construction, trade, transport and warehousing services and real estate activities.

A less favourable environment for the second quarter – and possibly beyond

STATEC highlighted that the signing on 17 June of a memorandum of understanding aimed at ending the conflict between the United States and Iran was welcomed as positive news. Equity markets reacted favourably, while oil prices declined (Brent crude returning towards USD 80 per barrel after comfortably exceeding USD 100 between March and May).

Nevertheless, the disruption caused by the closure of the Strait of Hormuz points to subdued economic activity in the second quarter and likely into the third quarter. Since March, business surveys have shown a marked deterioration in consumer confidence, against a backdrop of rising inflation driven mainly by higher fuel prices—two factors likely to weigh significantly on household consumption. Business confidence indicators, particularly in the services sector, have also fallen sharply across the euro area since March. The global supply chain pressure index, already rising at the beginning of 2026, increased substantially in April and May and has reached its highest level since mid-2022.

Even if shipping traffic resumes through the Strait of Hormuz, few expect an immediate return to pre-closure levels, owing in part to logistical constraints and the need to repair damaged infrastructure. Moreover, significant uncertainty remains regarding the eventual outcome of negotiations between the United States and Iran. This is likely to maintain upward pressure on prices and weigh on economic activity.

Monetary policy tightens in the Euro area

At its Governing Council meeting on Thursday 11 June, the European Central Bank (ECB) decided to raise its key interest rates by 25 basis points in response to growing inflationary pressures. Inflation in the euro area accelerated from 1.7% in January 2026 to 3.2% in May 2026, exceeding the ECB's 2% target. Energy prices, under pressure owing to the closure of the Strait of Hormuz, rose by 11% year-on-year and accounted for around one-third of the inflation recorded in May.

This tightening of monetary policy comes almost three years after the previous rate increase in September 2023. During the 2022–2023 energy crisis (triggered by the outbreak of war in Ukraine), the ECB waited until euro area inflation had reached nearly 9% before raising rates, taking them from 0% to 4.5% in less than eighteen months. Faced with this new inflationary shock, the ECB has chosen to act more swiftly. Although moderate for now, this increase in policy rates will result in higher variable mortgage rates and more expensive borrowing for businesses and consumers.

Labour market participation rate rising

STATEC reported that the labour force participation rate has increased significantly in Luxembourg since the end of 2024, indicating that a larger proportion of the working-age population is participating in the labour market. Growth in the labour force (residents in employment or registered with ADEM) strengthened last year (rising from +1.4% in 2024 to +1.7% in 2025), while population growth slowed (from +1.5% to +1.3%) following a decline in net migration.

This acceleration in labour force growth was initially driven by a rebound in employment. At the beginning of 2026, however, employment among residents slowed (with the vast majority of jobs created in Luxembourg being filled by cross-border workers), while the number of unemployed persons rose sharply.

It should be noted that the increase in the unemployment rate—from 6.0% in the third quarter of 2025 to 6.2% in May 2026—is explained by the rise in the number of unemployed individuals not receiving benefits. Combined with the higher participation rate, this suggests that part of the increase in unemployment reflects previously inactive individuals registering with ADEM.

Lower inflation thanks to Tripartite measures

In its latest inflation forecasts, STATEC projected, under its central scenario, inflation of 2.5% in 2026 and 1.7% in 2027, with a further wage indexation tranche expected in the second quarter of 2027, following that of June 2026. However, the measures contained in the Resilienzpak 2026, adopted through the tripartite agreement, are expected to reduce energy price growth to 2.3% in 2026, compared with 6.6% in the absence of such measures. This would result in overall inflation of 2.2% in 2026, 0.3 percentage points lower than under a no-measures scenario.

The central scenario, which already assumed the reopening of the Strait of Hormuz from May onwards, remains broadly valid regarding oil prices. Brent crude prices fell from a peak of around USD 125 per barrel at the end of April to USD 80 in mid-June, with the average price during the second quarter standing at USD 108 per barrel—closely aligned with the central scenario assumption of USD 113 per barrel.

The introduction of these measures does not alter the forecast timing of the next wage indexation tranche under the central scenario (Q2 2027), but it does reduce the risk of inflation accelerating sufficiently to bring forward indexation to the second half of 2026.

Varied energy support measures across Europe

STATEC said that with the tripartite agreement of Monday 8 June 2026, Luxembourg joined many other European countries that have introduced support measures in response to the war involving Iran and the resulting increase in energy costs. According to information compiled by Bruegel, EU countries are allocating around €12 billion to such measures (equivalent to 0.1% of EU GDP). In absolute terms, Spain is by far the largest contributor (more than €4.5 billion), while, as a percentage of GDP, Cyprus ranks first, ahead of Luxembourg. For Luxembourg, the entire tripartite agreement is included, even though some measures extend beyond the energy crisis itself (notably the increase in the tax credit linked to the social minimum wage and adjustments to income tax brackets).

Measures adopted across Europe include targeted support for transport, agricultural and fishing businesses. In addition, countries have either reduced taxes on fossil fuels or introduced assistance for households (primarily low-income households) to help offset higher energy costs. In Luxembourg, a temporary reduction in various energy prices has been introduced, covering both fossil fuels — as elsewhere in Europe — and electricity prices.

Falling oil prices: Is the crisis over?

The announcement in mid-June of the extension of the 60-day ceasefire and the reopening of the Strait of Hormuz by the United States and Iran led to a decline in oil prices and lower expectations for future prices. Despite the uncertainties still surrounding the agreement, both countries reported further progress in negotiations over the previous weekend, helping to reassure investors. Oil price expectations for 2026 have fallen by around USD 10 per barrel since the announcement, while futures prices for 2027 and 2028 have also declined. However, they remain above pre-conflict levels.

STATEC said several factors explain this situation. First, it remains difficult to assess how long it will take for navigation through the Strait of Hormuz to return fully to normal and how quickly producers will be able to restore output levels. Secondly, reserves that were drawn upon to cushion the impact of the crisis will need to be replenished gradually, supporting demand and therefore prices. The International Energy Agency has recently indicated that it expects the oil market to return to a surplus supply situation as early as 2027.