Credit: CSSF

Credit: CSSF

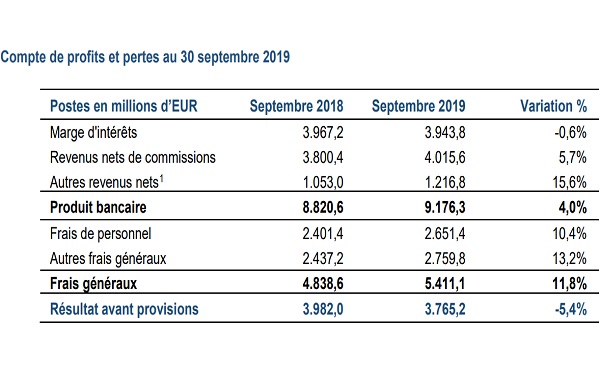

The Commission de Surveillance du Secteur Financier (CSSF) has announced that the profit before provisions of the Luxembourg banking sector was €3.765 million at the end of the third quarter of 2019.

As of 30 September 2019, Luxembourg credit institutions recorded a profit before provisions of €3.765.2 million, representing a decrease of 5.4% compared to the same period the previous year.

On the revenue side, the interest margin narrowed by 0.6% overall. However, half of the credit institutions saw a positive development of the interest margin thanks to the increased volume of activities and the improvement in the average rate of return on assets. The application by the European Central Bank (ECB) of negative interest rates on the deposit facility continued to pose a real challenge for credit institutions. In order to compensate for the negative interest paid on assets, some banks are now applying negative interest rates on deposits collected from professional customers and are gradually starting to extend this practice to very wealthy private customers.

Net commission income increased by 5.7%, thus reflecting the positive development of trades related to the management and custody of financial assets. However, only 45% of banks experienced an increase in their net commission income. In addition, the magnitude of this increase comes mainly from a few credit institutions whose growth in activity is strongly linked to Brexit.

As in previous quarters, general expenses continued to increase sharply (+11.8%). This increase affected both other general expenses (+13.2%) and personnel costs (+10.4%). Although the majority of banks were affected by an increase in overheads, the scale of this increase is mainly attributed to mobilisation of the human and technical resources necessary to manage banking activities being transferred in light of Brexit to a few credit institutions.

Such developments have led to a deterioration in the expense-to-income ratio which rose from 55% to 59% at the end of the third quarter of 2019. This unfavourable trend reflects the difficulty of banks in maintaining profitability.