Credit: Pixabay

Credit: Pixabay

On Thursday 21 December 2023, Luxembourg's Ministry of Housing and Regional Planning reported that the "Analysis report 9" just published by the Housing Observatory takes stock of developments in activity, sales prices and rents announced for residential real estate in the 3rd quarter of 2023.

In summary, the level of activity remains much lower than in previous years across all residential real estate and land segments: the number of sales is down -31.9% compared to the 3rd quarter of 2022 for existing apartments, -47.3% for existing houses, -56.4% for building land and finally -59.9% for apartments under construction.

At the same time, sales prices are down very sharply this quarter: -13.6% compared to the 3rd quarter of 2022 according to the Statec hedonic index. The drop in prices is observed across all segments, even if price developments remain heterogeneous: -7.7% for apartments under construction, -12.3% for existing apartments and -18.7% for existing houses.

On the rental market, (announced) apartment rents have stabilised for two quarters. The increase in (announced) rents, however, remains clear over twelve months: +4.1% for apartments and +4.0% for houses between the 3rd quarter of 2022 and the 3rd quarter of 2023, almost identical to that of measured consumer prices by the IPCN (+4.0%) over the same period.

The findings in detail:

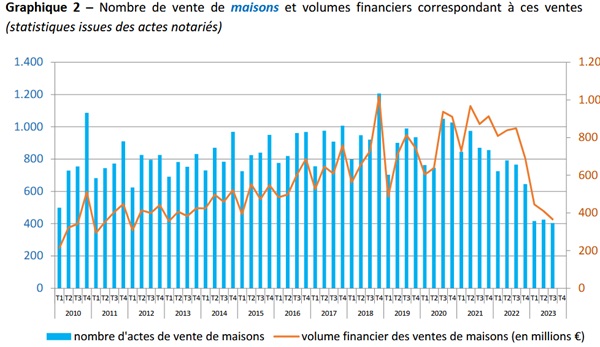

a. Number of housing sales

Activity in the real estate and residential land markets remains, in the 3rd quarter of 2023, at levels much lower than those recorded in previous years, and this affects all segments. For apartments under construction, existing houses and building land, this is the lowest number of sales recorded over a quarter since the creation of the land registration file in 2007.

It is in the apartments under construction (VEFA) segment that the number of transactions has fallen most sharply for three quarters, reaching only 119 sales this quarter (-59.9% compared to the 3rd quarter of 2022). The number of transactions is thus more than 5 times lower than the average for the years preceding the health crisis (671 sales of apartments under construction in the 3rd quarter on average over the years 2017 to 2019).

b. Real estate prices

The housing sales price index provided by Statec (including both existing housing and housing under construction) fell by 13.6% between the 3rd quarter of 2022 and the 3rd quarter of 2023.

The drop in prices observed since the start of 2023 continues and is increasing very sharply for existing housing: -12.3% for existing apartments and -18.7% for existing houses. This drop in prices is particularly marked for houses, which are obviously the most expensive goods, for which the drop in household purchasing capacity linked to the sharp rise in interest rates seems to have had the most significant effect.

Unlike the previous quarter, the sales prices of apartments under construction (VEFA) are also affected by a very clear drop over twelve months (-7.7%), driven by a sharp decrease in prices over the quarter. It therefore seems that certain developers have chosen to lower prices (or have been forced to do so) in the 3rd quarter of 2023, contrary to what has been observed until now. However, the number of transactions remains very limited in this segment, which suggests that other developers have probably chosen to wait further, by not reducing their marketing prices.

c. Announced rents

After several quarters of sharp increases, announced rents (from real estate advertisements) have stabilised for two quarters. The increase in announced rents, however, remains clear over twelve months: +4.1% for apartments and +4.0% for houses between the 3rd quarter of 2022 and the 3rd quarter of 2023. The increase in announced rents over twelve months is as follows: almost identical to that of consumer prices measured by the IPCN (+4.0%) over the same period.

In the rather specific segment of furnished room rentals, which currently represents around 12% of the total rental supply, the increase in announced rents is a little high: +4.6% over twelve months.

The increase in (announced) rents noted over twelve months is undoubtedly explained by a shift of part of the demand from ownership to rental. However, the stabilisation observed over the past two quarters reflects the existence of a strong constraint on rents: tenants' incomes have not increased enough to absorb too sharp an increase in rents requested by landlords.

Finally, it should be noted that these are the rents requested for new rental contracts. The increase in rents during the lease (for tenants who do not change accommodation) is much more moderate, very significantly lower than inflation on consumer goods: only +1.7% for the rental index. Statec rents between the 3rd quarter of 2022 and the 3rd quarter of 2023.

Note: The analysis report 9 is based on data collected by Statec and the Habitat Observatory, in collaboration with the Registration, Domains and VAT Administration, with regard to the activity and the sale prices of housing (from notarial deeds). It also uses data provided by the real estate portal Immotop.lu regarding the announced rents of housing (from real estate advertisements).