Credit: STATEC

Credit: STATEC

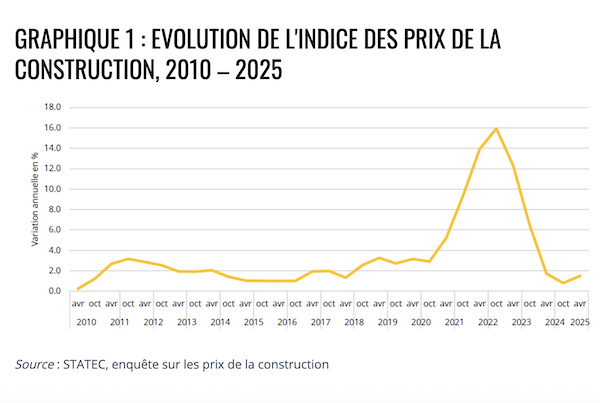

On Wednesday 16 July 2025, Luxembourg's national statistics agency STATEC reported that residential construction prices rose by 1.3% between October 2024 and April 2025, following two semesters of limited growth.

According to STATEC, following the sharp increases seen in 2021 and 2022, price developments are gradually returning to their long-term average growth rate of 1.0%, as observed between 2010 and 2019. This recovery affects all construction trades, with residential construction prices rising by 1.5% over the past year.

STATEC reported that the downward trend in structural work prices observed in 2024 has come to an end, with masonry work seeing a renewed increase of 0.9%. This development reflects slight price rises in materials such as reinforcing steel and sand, which have been passed on to project owners. Nevertheless, structural work remains the trade with the lowest half-yearly change, while earthwork prices remained almost unchanged (-0.1%).

Roofing works recorded the sharpest rebound, with prices climbing by 2.0%, significantly influencing the overall index. STATEC noted that this trend was partly driven by increased prices for wood, insulation materials and other supplies such as roof windows and tiles. Timber frames rose by 1.7%, insulation works by 2.1%, and roof coverings by 2.3%. Overall, roofing remains the most affected trade since the start of the materials crisis and inflationary surge, with a 45.5% increase between 2020 and April 2025.

Building closure works, including windows with solar protection, garage doors and facade, saw a price rise of 1.7% between October 2024 and April 2025. STATEC added that the cost of exterior joinery for residential buildings increased by 2.1%, while facade work rose by 1.3%.

Technical installations continued to grow at a steady pace (+1.5%), following already dynamic semesters (+2.5% and +1.1%). All segments contributed to this trend: sanitary installations (+1.9%), heating and ventilation systems (+1.3%) and electrical installations (+1.6%). This sustained growth was mainly attributed to higher supply prices passed on to clients.

Finishing works also rebounded, albeit to a lesser extent. STATEC highlighted that only painting (+3.0%), floor coverings (+1.9%) and screeds and coatings (+1.6%) exceeded the general index of +1.3%. Other services, such as tiling (+0.0%) and plastering (+0.4%), remained stable or showed only marginal increases. Excluding structural works, finishing trades saw the lowest annual change in prices (+1.4%).

The general composite index for April 2025, expressed on a base of 100 in 1970, stands at 1164.15 points. This index is used for the indexation of almost all fire insurance contracts, as well as for many other applications such as the updating of estimates or sales contracts in future state of completion.

The construction price index measures price changes (excluding VAT) of services provided in residential construction, excluding land. It takes into account changes in the prices of materials and labour, as well as variations in productivity and contractors' margins. Indices and variation rates are calculated half-yearly for construction as a whole, and also for different trades and groups of services.

This index is published twice a year, in January for data from October of the previous year and in July for data from April.