Credit: STATEC

Credit: STATEC

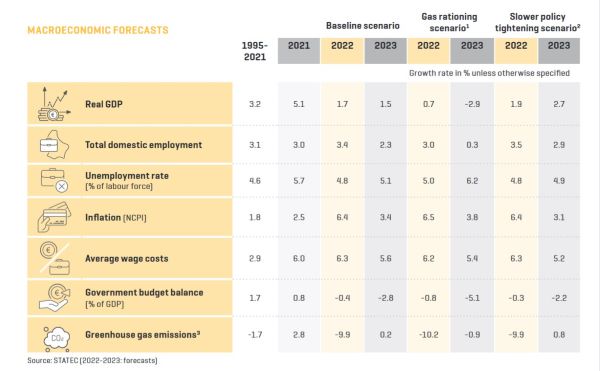

Luxembourg’s national statistics institute STATEC recently published a report on the macroeconomic outlook of Luxembourg's economy for 2023, which it anticipated would grow only moderately.

According to STATEC's forecast, Luxembourg could experience GDP growth of less than 2% in 2022 (1.7%) and again in 2023 (1.5%) and public deficit could reach 3% of GDP in 2023.

STATEC explained that against the backdrop of intense pressure on energy prices and the sharp rise in inflation, economic activities have been negatively impacted. Mainly driven by the impact of the war in Ukraine on energy costs, historically high inflation continues to rise across Europe.

This energy crisis follows the COVID-19 pandemic and poses many challenges. In Europe, measures have been taken to limit the increase in household energy bills and gas supply disruptions. Monetary policies in most developed economies have been tightened in order to reduce inflation, which will restrict financing for economic actors and increase the risks related to high levels of debt.

According to STATEC, activity in the euro area remained solid in the first half of 2022. However, the third quarter was marked by a clear slowdown. Business and household confidence continued to deteriorate as winter approaches, thus pointing towards an even more challenging end of 2022 and start of 2023. In the euro area, GDP is expected to stagnate in 2023, after growing by 3% this year.

Activity in Luxembourg fell in the second quarter of 2022, affected in particular by the negative performance of manufacturing and construction. These two branches experienced supply chain issues in 2021 and witnessed a drop in demand this year. The financial sector held up better in the second quarter, but its added value in the first half of the year was lower than in the first half of 2021, with the results of financial auxiliaries affected by the deteriorating stock market environment. While the current rise in interest rates may represent an opportunity for banks to increase earnings, it has been accompanied by a fall in demand for loans, combined with stricter lending conditions.

STATEC cautioned that the outlook for the second half of 2022 is bleak, with surveys pointing towards a further deterioration in the business atmosphere coupled with highly negative signals for household consumption, in particular concerns about high inflation. The measures to counter the effects of rising energy prices, negotiated under the tripartite agreements, will serve as a major support for the purchasing power of households and the businesses in Luxembourg affected by the energy crisis. Economic activity should therefore continue to rise, but on a very modest growth trajectory, with real GDP growth expected at 1.7% this year, then 1.5% in 2023.

2022 has been marked by historically high levels of inflation, although it is less pronounced in Luxembourg than elsewhere in the European Union (EU). This surge in inflation is the result of a combination of factors ranging from global supply bottlenecks, increased demand resulting from a "return to normal" after two years of health restrictions, tensions on the energy market amplified by the war in Ukraine and the appreciation of the US dollar, which automatically raises the price of several imported goods.

The delayed impact of soaring energy prices on all other prices, especially food prices, is putting strong upward pressure on inflation in Luxembourg, confirmed STATEC. This effect is reinforced by the depreciation of the euro, which looks set to last longer than previously anticipated. These developments have led STATEC to revise its inflation forecasts upwards.

In line with high inflation, the compensation per employee showed strong growth in the second quarter of 2022 in the euro area and Luxembourg. Over the year as a whole, the compensation per employee is expected to increase by 6.3% in Luxembourg in 2022, and by 5.6% in 2023, under the major effect of successive wage indexations. Real household disposable income per capita is expected to stagnate in 2022 and to increase by about 2% in 2023, with the purchasing power of low-income households being significantly supported by the measures agreed in the tripartite negotiations.

While job creations remained relatively high in the euro area and in Luxembourg in autumn 2022, they have clearly entered a period of slowdown. The unemployment rate, even if it remains low, has recently resumed an upward trend in Luxembourg (as well as in several countries of the euro area). Business employment prospects, as well as other leading indicators of employment, have worsened during 2022, leaving little doubt that unemployment will continue to rise, underscored STATEC. However, this increase should be moderate, with the proportion of vacancies still at a historically high level.

During 2022, the labour market was still buoyed by the post-pandemic recovery. However, the outlook for 2023 is gloomier. The near-stagnation in activity forecast for the euro area will also be accompanied by a sluggish employment market. In Luxembourg, the slowdown in activity would be less marked but would still lead to a slowdown in employment (from an increase of 3.4% to an increase of 2.3% in 2022) as well as a slight rise in unemployment (to 5.1% of the labour force, compared to 4.8% in 2022).

In 2022, tax revenues in Luxembourg were boosted by the effects of high inflation on VAT revenues, household taxes and social contributions. However, there has been a slowdown in revenue growth since the second quarter of 2022, due to weaker fuel sales and the stock market pullback. The slowdown should accentuate in 2023 with the reduction in VAT rates, a less buoyant property market and, in general, a more subdued economic climate.

Government spending has increased strongly in 2022, driven by growth in employment, wages, pensions and operating costs. Spending growth is expected to be even stronger in 2023, partly as a result of measures introduced to curb high inflation and to help households and businesses particularly affected by rising energy prices.

The nominal balance will then deteriorate from a decrease of 0.4% of GDP in 2022 to a decrease of 2.8% in 2023. This is a sharp downward revision from previous forecasts. However, it reflects the weaker economic climate and the measures taken as a result of this situation.

Energy markets are in turmoil, generating high price volatility. Largely due to the war in Ukraine, gas and electricity prices reached historically high levels this summer, while oil prices returned to levels not seen since 2014. These developments have threatened the purchasing power of households and raised costs for companies. On the other hand, the fossil fuel crisis could accelerate the energy transition.

Two tripartite negotiations were held in Luxembourg within six months to implement measures to mitigate rising energy bills and inflation in general. Anticipating a potential shortage of gas, and even electricity, the EU has issued recommendations to member states to guarantee supply, with targets for storage and consumption reductions. A mild winter start has also helped to lessen the risk of shortages. Luxembourg consumed significantly less gas over the first nine months of 2022 compared to the average of the previous five years (down 19%, compared to a decrease of 7% in the EU). The surge in energy prices in 2022 has therefore had a resounding impact on consumption. On the other hand, the aid measures taken in neighbouring countries have temporarily removed the competitive advantage of Luxembourg's petrol prices, leading to a fall in fuel sales. Greenhouse gas (GHG) emissions have thus decreased by 10% in 2022, falling below the level witnessed in the crisis year 2020.