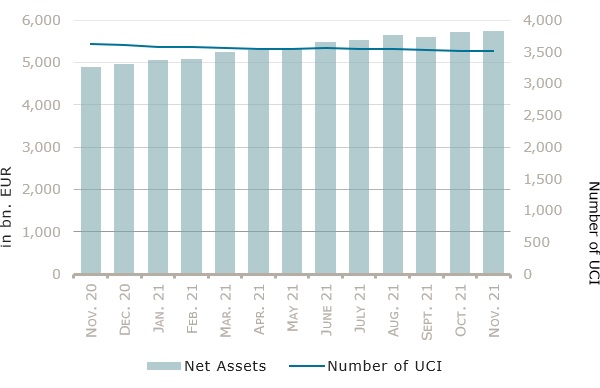

On Tuesday 28 December 2021, the Commission de Surveillance du Secteur Finance (CSSF), Luxembourg's financial regulator, confirmed that, as at 30 November 2021, the total net assets under management by entities in the Grand Duchy amounted to €5,749.910 billion compared to €5,718.484 billion as at 31 October 2021, i.e. an increase of 0.55% over one month; over the last twelve months, the volume of net assets rose by 17.77%.

These assets are of undertakings for collective investment (UCIs), comprising UCIs subject to the 2010 Law, specialised investment funds and SICARs.

The Luxembourg UCI industry thus registered an increase of €31.426 billion in November 2021: this increase represents the sum of positive net capital investments of €29.802 billion (+0.52%) and of the positive development of financial markets amounting to €1.624 billion (+0.03%).

The development of undertakings for collective investment is presented in the image above.

The number of UCIs taken into consideration totalled 3,508, against 3,518 the previous month. A total of 2,303 entities adopted an umbrella structure representing 13,250 sub-funds. Adding the 1,205 entities with a traditional UCI structure to that figure, a total of 14,455 fund units were active in the financial centre.

As regards the impact of financial markets on the main categories of undertakings for collective investment and the net capital investment in these UCIs, the following can be said for the month of November:

The emergence of a new COVID-19 variant and the more persistent than expected inflation in the US and Europe weighted on investor sentiment. Against this backdrop, equity markets fell over the month while government bonds rallied.

Concerning developed markets, the European equity UCI category registered a negative performance in a context marked by rising hospitalisations and new restrictions induced by the fourth COVID-19 wave in several European countries, a higher inflation rate in the euro area as well as the persistent supply chain shortages. While US shares declined in November amid concerns about the Omicron variant of COVID-19 and the possibility of a swifter tapering of the asset purchases by the Federal Reserve (Fed) in light of the sharp pick-up of inflation, the strong appreciation of the USD against the Euro shifted the US equity UCI category into positive territory. The Japanese equity UCI category fell as well in consequence of the short-term uncertainty over the new Covid-19 variant, despite a substantial fiscal stimulus package initiated by the new Japanese government and the strong appreciation of the Yen against the EUR.

As for emerging countries, the Asian equity UCI category declined overall under the impulse of concerns that the emergence of the Omicron variant could hurt global economic recovery and falling Chinese equity markets amid fears of new lockdown measures as this new COVID-19 variant spreads rapidly in China, a slowing property market and ongoing regulatory scrutiny of the internet industry. The Eastern European equity UCI category was sharply lower, mainly on the back of falling oil prices and a resurgence in COVID-19 cases in the Czech Republic, Hungary and Poland. The Latin American equity UCI category realised in overall a negative performance in November largely due to a decline of the Brazilian and Mexican equity markets on the grounds of higher inflation.

In November, the equity UCI categories registered an overall positive net capital investment, mainly driven by inflows in the Global market equity UCI category.

Concerning the EUR and USD denominated bond UCI categories, the long-term yields of government bonds declined (i.e. bond prices increased) as demand for safe-haven assets surged amid higher Omicron-related uncertainty. While the European Central Bank (ECB) will take a decision on the continuity of its “Pandemic Economic Purchase Program” (PEPP) in December, the US Federal Reserve (Fed) considers accelerating the pace of tapering. Against this backdrop, US and European investment grade corporate bonds tracked sideways. Overall, the EUR and USD denominated bond UCI categories finished the month in positive territory. The USD denominated bond UCI category was further supported by the appreciation of the USD against the EUR.

The emerging market bond UCI category recorded negative returns, under the impulse of the US Fed’s shift toward a more hawkish stance, concerns that the spread of the new COVID-19 variant could have an adverse effect on global supply chains and idiosyncratic risks in some emerging markets.

In November, fixed income UCI categories registered an overall positive net investment, mainly driven by the EUR and USD money market UCI categories.