Depositary banking market concentration;

Credit: ABBL

Depositary banking market concentration;

Credit: ABBL

In order to gain a better understanding of the depositary and custodian banking sector in Luxembourg, the Luxembourg Bankers' Association (Association des Banques et Banquiers Luxembourg - ABBL) has launched a first national survey on these industries in collaboration with Luxembourg's financial regulator, the Commission de Surveillance du Secteur Financier (CSSF).

The study sheds a light on two professions with which many people may be unfamiliar. Its results, which concern the 2021 figures, highlight the good health of these trades.

"Often seen as a single business, sometimes carried out by the same players, depository and custodian banking nevertheless deal with different clients and are subject to different obligations", explained David Claus, Chair of the ABBL's Depositary Banking Cluster and CEO of European Depositary Banking SA.

Custody is the "traditional" activity of depositing and holding securities on behalf of third parties. This activity has evolved over time depending on the clients for whom it was provided, particularly in the case of investment funds, where its scope significantly increased due to the adoption of dedicated sectoral standards (AIFM and UCITS directives). In these cases, the activity is referred to as depositary, which covers the activity of custody and safekeeping, but is also accompanied by other obligations such as supervision and control, as well as a specific liability regime in this area.

"In a nutshell, depositary banking addresses the fund industry", said Christian Dominique, Vice-chair of the ABBL's Depositary Banking Cluster and Head of Client Delivery and Chief Operating Officer at BGL BNP Paribas Securities Services. More specifically, the following vehicles are concerned: UCIs / investment vehicles with depositary requirements, such as UCITS, Part II funds, SIFs, SICARs, RAIFs, unregulated company qualifying as AIF and having appointed a depositary, but also non-Luxembourg domiciled investment vehicles with depositary requirement as per article 36 of the AIFMD.

"Whereas custodian banking services concern [all] other clients", added Christian Dominique. In particular, the study made it possible to obtain a more granular view of the clienteles concerned by this sector: pension schemes and funds, global custodian services, banks and bank deposits, corporate clients, insurance funds and private and public issuers.

"It is worth mentioning that having a depositary bank acting in the investors interest as further gatekeeper, alongside the national supervisory authorities, the fund's management bodies and the auditors, is a European specificity", stressed Eric Guerrier Vice-chair of the ABBL's Depositary Banking Cluster and Head of Depositary Oversight & Custody Diligence at Pictet & Cie (Europe) SA. In this context, the depositary bank plays a key role, according to ABBL, as it is in the best position to monitor the fund’s activity on an ongoing basis and to intervene in case of discrepancies or irregularities.

In Luxembourg, the depositary bank business has developed in parallel with the growth of the investment fund industry. It kickstarted in 1988, when the country was a first mover to transpose the UCITS Directive. In 2021, the industry represented €6.5 trillion assets under deposit (AuD). The 22% growth compared to 2020 was mainly due to market performance. In the same period and for the same reasons, the custodian banking sector also grew, with assets under custody (AuC) up to €5.5 trillion (+15%).

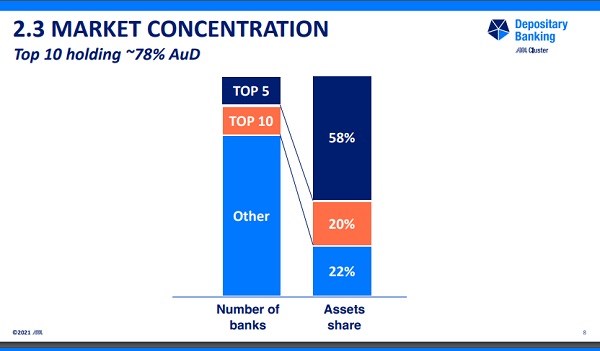

Both markets are heavily concentrated with the top 10 players holding approximately 78% of AuD in one industry and around 88% of AuC in the other. Staff numbers have been constant with 953 full-time employees working in depositary supervision functions and 1,204 in custody and safekeeping operations, thus representing around 10% of total banking staff working in Luxembourg.

"If 2021, was a very good year, 2022 will be of a different kind", admitted David Claus. Like other sectors of the financial industry, the depositary and custodian banking industries are dependent on the geopolitical and economic environment that affects the financial markets. In addition, there are the effects of inflation, as well as the specific Luxembourg context of salary indexation. Legislative challenges are also ahead, with the UCITS and AIFMD directives due to be recasted and the shoulders of professionals in these sectors potentially having to bear the burden of even more obligations.

"Finally attracting and keeping skilled talents are challenges, like for many Luxembourg based companies, but even more so as our trades are getting more and more specialised as we continuously deal with new categories of assets", said Eric Guerrier.

However, as David Claus noted: "Looking further ahead, we remain positive about the future of our businesses. Even in the face of the opportunities and challenges posed by the advent of sustainable finance and the emergence of crypto-currencies, we remain convinced that the Luxembourg fund industry, and therefore the Luxembourg depositary banking industry, are very well positioned to face international competition. Strong and competent monitoring will always be seeked for, whatever the underlying asset are. And that is what our industry stands for".

Regarding the use of DLT technologies, the leaders of the ABBL cluster remain confident that it will not "disenfranchise" their businesses. "We believe that DLT will not be used on processes for which we already have an excellent track record in standardisation and streamlining. On the other hand, on assets such as private equity or real estate where this has not been possible so far, we expect it to add a lot of value", concluded Christian Dominique.

A total of 53 banks participated in this study, meaning a 100% coverage ratio. Non-banking depositaries were not included in the survey.