Credit: STATEC

Credit: STATEC

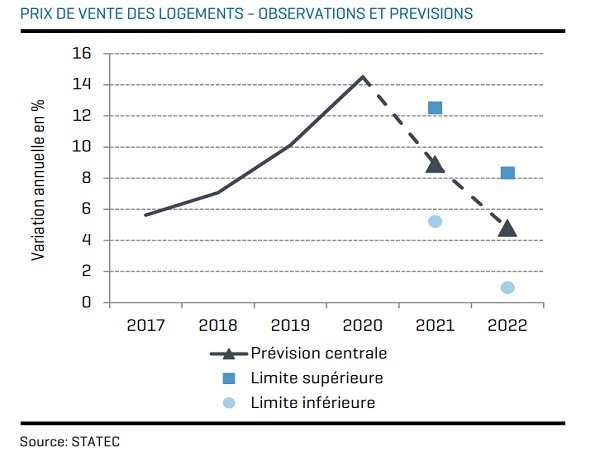

In its latest report, Luxembourg's statistical institute, STATEC, has forecast a potential slowing down in house price increases in the Grand Duchy in the next two years.

STATEC noted that housing prices have accelerated markedly in recent years. In 2019, and even moreso in 2020, the observed price increases were greater than what their usual determinants indicate. This mismatch could be corrected in 2021 and 2022 and lead to less pronounced increases, although these forecasts contain a significant margin of uncertainty.

In Luxembourg, the rise in property prices has been accelerating for ten years and peaked in 2020, with a 14.5% increase - one of the highest increases ever recorded.

In its recent study, STATEC focused on the econometric identification of the determinants of property prices. Finding an equation that manages to explain a large part of price fluctuations using economically relevant and significant determinants should notably allow to judge the existence or not of a speculative bubble and to make predictions.

On the basis of data observed between 1980 and 2020, real estate prices depended primarily on two other prices: those of building land and those of residential investment (or new construction) excluding land.

The real estate market is governed by supply and demand - and four major variables play a role here: the ratio between the population and the stock of residential capital (indicator of tension); the number of households (which is growing faster than the population); the number of buildings completed per year (gross supply); the mortgage interest rate deflated by consumer prices (financial cost).

Finally, two financial variables reflect the choice available to an investor (buying a home and renting it, for the purpose of yield, or acquiring financial products): the Euro Stoxx 50 stock market index (a rapid rise in stock market values curbs residential investment) and the gao between long and short rates (the higher it is, the higher the interest for a financial investment should be).

STATEC found that there was no speculative bubble but a significant overvaluation in Luxembourg in 2020. The main conclusions of the study were as follows:

- it is not appropriate to speak of a "speculative bubble" because the fundamentals manage to explain nearly 80% of the fluctuations real estate prices have observed since 1980;

- 2019 and especially 2020 are exceptions in this regard: property prices were higher in 2019 than what follows from the fundamentals, but this difference was not greater than during other overvaluation phases;

- on the other hand, 2020 was marked by a significant overvaluation, which can be estimated at around 5%;

- using the estimated equation, STATEC established a forecast of real estate prices for 2021 (+ 9%) and 2022 (+ 5%);

- the deceleration compared to 2020 would come from the fact that the exceptional (unobserved) factors that led to the rise in prices would gradually disappear and the upward movement would then be in line with the fundamentals, marked above all by a structural excess of demand for the offer.

In addition, STATEC noted that Luxembourg got off to a good start to the year in the first quarter of 2021: real GDP increased by 1.4% over one quarter. While the euro zone as a whole fell back into recession at the crossroads of 2020 and 2021 under the effect of the new pandemic wave and the tightening of restrictions, Luxembourg's GDP continued to grow. It was mainly sustained over this period by the increase in added value from the financial sector and information and communication services.

At the end of the first quarter of the year, the growth rate for 2021 thus amounts to 5.5% (i.e. under the assumption that GDP stabilises at the level of the first quarter over the remainder of the year, excluding revisions on previous quarters). In this regard, the 6% growth envisaged for this year seems largely within reach. Activity in Luxembourg and in Europe is expected to regain momentum from the second quarter in connection with a continued easing of restrictions.

Industrial production in Europe and Luxembourg has tended to return to its pre-crisis levels since the start of the year. Demand seems to be there, but there are constraints weighing on supply, with manufacturers citing supply difficulties for certain basic or intermediate products. To meet demand, they have therefore had to draw heavily on their stocks. However, not all areas of industry are affected by the phenomenon. In Luxembourg, manufacturers consider their stocks insufficient namely in the areas of wood products, paper, rubber and plastic and computer, electronic, optical and electrical products.

At the end of the first quarter of 2021, the assets of European investment funds had climbed to more than €19 trillion (up 4.5% over one quarter, up 25% over one year), driven mainly by stock market valuations, but also by net emissions. A third of the increase at the start of the year came from collective investment undertakings in Luxembourg, the European leader which holds 27% of assets.

The public sector (in the broad sense) has been the main source of job creation over the past year, both in Luxembourg and in the euro area as a whole. However, the Grand Duchy stands out positively from other eurozone countries, with employment growth of 5% in this sector, compared to 0.7% growth for the eurozone as a whole. The public sector thus contributed 1.1% (out of 2.0%) of employment growth in the Grand Duchy in 2020, compared to 0.2 of employment growth in the euro area (where overall employment fell by 1.6%).

STATEC also noted that the upward trend in greenhouse gas emissions from 2017 to 2019 was broken in 2020 by the fallout from COVID-19. The statistical institute expects emissions to fall by 17% in 2020, mainly due to the collapse of freight transport in the Eureopean Union, which has contributed to lower fuel sales. While Luxembourg has met its climate objectives for 2020, it should expect a rebound (albeit limited by the CO2 tax) in emissions from 2021. The extent of this rebound will depend on the scenario for exiting the crisis, in Luxembourg but above all at European level. A rapid and substantial recovery in economic activity would induce a more pronounced rise in emissions.